Get Pre-Approved Now

How Does the CMHC Premium Hike Affect Your Second Mortgage Application?

Use the Code Below to Embed this Infographic into Your Website!

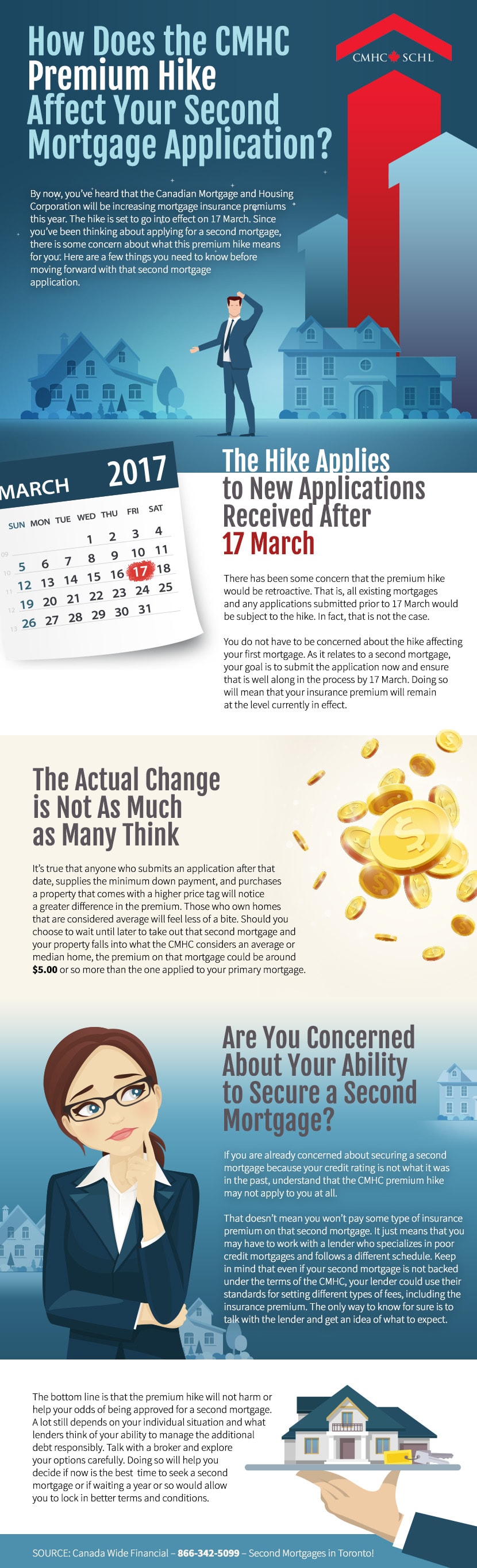

By now, you’ve heard that the Canadian Mortgage and Housing Corporation will be increasing mortgage insurance premiums this year. The hike is set to go into effect on 17 March. Since you’ve been thinking about applying for a second mortgage, there is some concern about what this premium hike means for you. Here are a few things you need to know before moving forward with that second mortgage application.

1. The Hike Applies to New Applications Received After 17 March

There has been some concern that the premium hike would be retroactive. That is, all existing mortgages and any applications submitted prior to 17 March would be subject to the hike. In fact, that is not the case.

You do not have to be concerned about the hike affecting your first mortgage. As it relates to a second mortgage, your goal is to submit the application now and ensure that is well along in the process by 17 March. Doing so will mean that your insurance premium will remain at the level currently in effect.

2. The Actual Change is Not As Much as Many Think

It’s true that anyone who submits an application after that date, supplies the minimum down payment, and purchases a property that comes with a higher price tag will notice a greater difference in the premium. Those who own homes that are considered average will feel less of a bite. Should you choose to wait until later to take out that second mortgage and your property falls into what the CMHC considers an average or median home, the premium on that mortgage could be around $5.00 or so more than the one applied to your primary mortgage.

3. Are You Concerned About Your Ability to Secure a Second Mortgage?

If you are already concerned about securing a second mortgage because your credit rating is not what it was in the past, understand that the CMHC premium hike may not apply to you at all. That doesn’t mean you won’t pay some type of insurance premium on that second mortgage. It just means that you may have to work with a lender who specializes in poor credit mortgages and follows a different schedule. Keep in mind that even if your second mortgage is not backed under the terms of the CMHC, your lender could use their standards for setting different types of fees, including the insurance premium. The only way to know for sure is to talk with the lender and get an idea of what to expect.

The bottom line is that the premium hike will not harm or help your odds of being approved for a second mortgage. A lot still depends on your individual situation and what lenders think of your ability to manage the additional debt responsibly. Talk with a broker and explore your options carefully. Doing so will help you decide if now is the best time to seek a second mortgage or if waiting a year or so would allow you to lock in better terms and conditions.